What is the Hyperliquid DEX?

Let us start with the one-sentence version, because the jargon piles up quickly. The Hyperliquid DEX is a decentralised exchange where you can trade perpetual futures and spot crypto without handing your money to a company. "DEX" simply stands for decentralised exchange: a trading venue that runs on a public blockchain rather than inside a private corporate database. You interact with it by connecting a self-custody wallet — the same way you might connect to Uniswap — and your funds stay under your own keys until you place a trade.

The word that does the heavy lifting here is non-custodial. On a custodial exchange — Binance, Coinbase, CEX.IO and the like — the company holds your assets for you, the way a bank holds your cash. On Hyperliquid, nobody holds your assets but you. There is no account to open, no password to reset, and no support desk that can freeze or unfreeze your balance. That is the defining feature of a DEX, and it is the source of both its appeal and its sharpest risks. We will come back to that repeatedly, because misunderstanding it is how newcomers lose money.

The second thing that sets Hyperliquid apart is that it is not just an app sitting on top of an existing chain like Ethereum. It is built on its own layer-1 blockchain — a base network engineered specifically to run a fast, fully on-chain order book. Most people describe Hyperliquid as "a chain, not just an app," and that framing is useful: the matching engine, the settlement and the smart-contract environment are all part of one purpose-built system. We will look at those layers — HyperCore and HyperEVM — a little further down.

One more piece of vocabulary before we go deeper. The network has a native token called HYPE, used for staking, governance and various fee-related mechanics. You do not need to own HYPE to understand the DEX, and we cover it separately in the HYPE token guide. For now, just file it away as "the network's own token."

CLOB vs AMM: why this design is unusual

To understand why Hyperliquid is interesting, you need to understand the two ways a decentralised exchange can match buyers with sellers. They sound technical, but the underlying ideas are simple.

The first model, used by Uniswap and most DeFi, is the automated market maker (AMM). There is no order book at all. Instead, people deposit pairs of tokens into a shared liquidity pool, and a mathematical formula sets the price based on the ratio of tokens in that pool. When you trade, you are not matched against another trader — you are trading against the pool, and the formula moves the price as you do. AMMs were a genuine breakthrough because they let a token trade 24/7 without anyone needing to post orders. But they are clumsy for serious trading: large orders suffer "slippage" (the price slides against you), and the model was never designed for leveraged products.

The second model is the central limit order book (CLOB) — the model every traditional stock exchange and every major centralized crypto exchange uses. Buyers post bids (the price they are willing to pay) and sellers post asks (the price they want), and a matching engine pairs them when prices cross. This gives you tight spreads, precise limit orders and proper price discovery. The catch: running an order book is computationally demanding, which is exactly why almost no DEX had managed to put a full order book on-chain. Most "on-chain order books" historically kept the matching off-chain and only settled trades on-chain.

Hyperliquid's distinguishing claim is that it runs the entire order book on-chain — order placement, matching and settlement — on a chain built for that workload. That is the unusual part. You get the trading experience of a centralized venue with the verifiability of DeFi. The comparison below lays out the trade-offs.

| Aspect | On-chain order book (Hyperliquid) | AMM DEX (Uniswap-style) |

|---|---|---|

| How prices are set | Buyers and sellers post bids/asks; a matching engine pairs them | A formula sets price from the ratio of tokens in a pool |

| Who you trade against | Other traders, via the order book | The liquidity pool itself |

| Order types | Limit, market and conditional orders | Effectively market orders only |

| Spreads & slippage | Tight spreads; large orders fill against resting liquidity | Slippage grows with order size relative to pool depth |

| Suited to leverage / perps | Yes — designed around derivatives trading | Poorly; AMMs were built for spot swaps |

| Verifiability | Orders, matches and liquidations are on-chain | Swaps and pool state are on-chain |

| Complexity to run | High — needs a purpose-built, high-throughput chain | Low — a smart contract on any EVM chain |

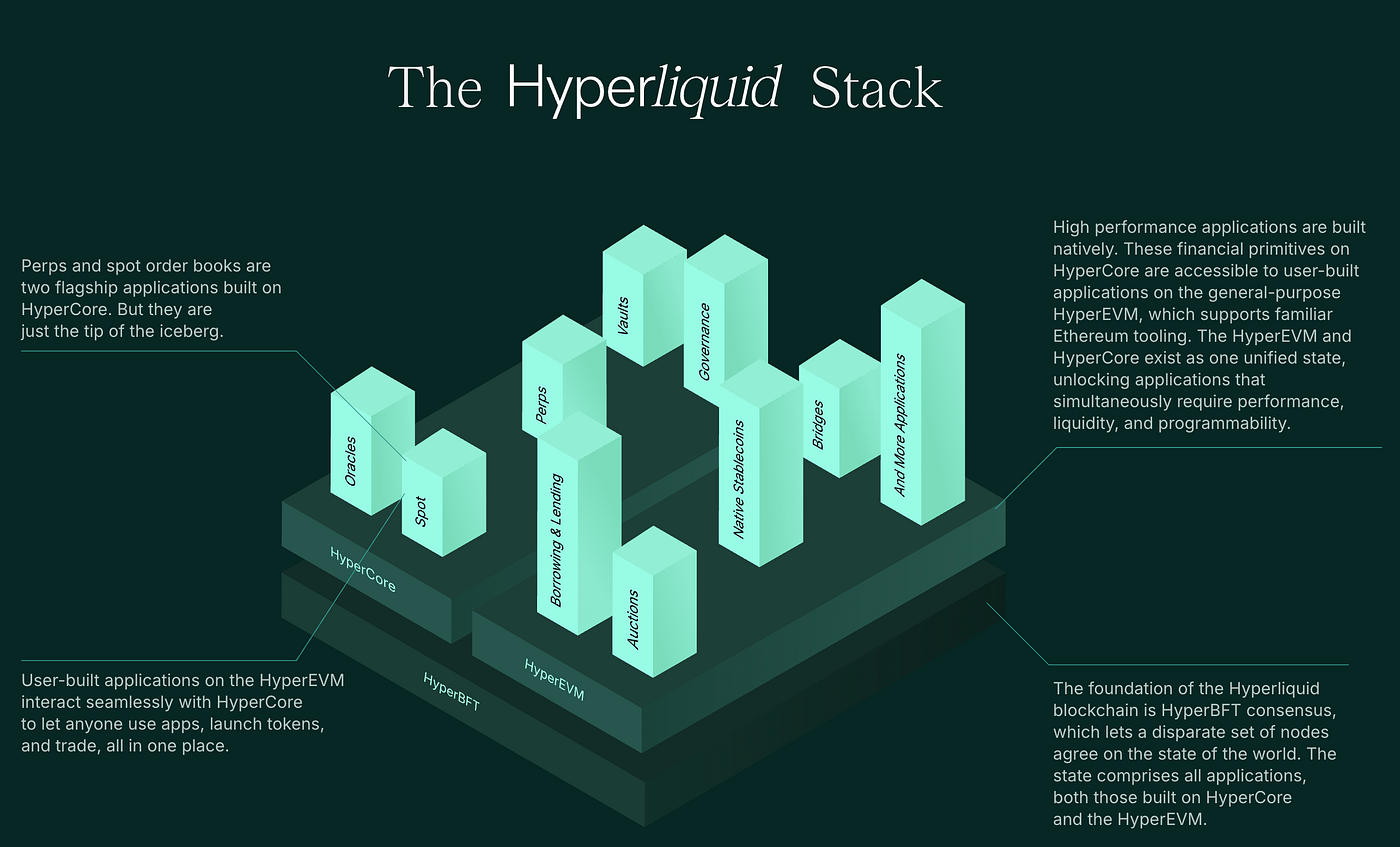

HyperCore and HyperEVM, explained simply

When people say Hyperliquid is "a chain, not just an app," they are usually pointing at two layers with slightly intimidating names. You do not need to memorise them to trade, but knowing what each does makes the rest of the ecosystem far less mysterious.

HyperCore is the engine room. It is the high-performance part of the chain that runs the order books and handles settlement — the perpetuals and spot markets, the matching, the margin and the liquidations all live here. Think of it as the trading floor: purpose-built, fast, and narrowly focused on doing one job extremely well. This specialisation is precisely why Hyperliquid built its own chain rather than deploying on an existing one — a general-purpose blockchain shared with thousands of other apps cannot offer the throughput and latency a live order book demands.

HyperEVM is the general-purpose neighbourhood next door. "EVM" stands for the Ethereum Virtual Machine — the standard environment that Ethereum and most smart-contract chains use. By offering an EVM-compatible layer, Hyperliquid lets developers deploy familiar smart contracts and applications that can tap into the same liquidity and assets that live on HyperCore. In plain terms: HyperCore is the exchange engine, and HyperEVM is where a broader ecosystem of apps can be built around it.

The reason this matters to you as a reader is simple. A purpose-built chain is what allows the fully on-chain order book to exist at all, and the EVM layer is what lets the project grow beyond a single exchange into a platform. The diagram below summarises how the pieces stack up.

Perpetuals vs spot — know what you're trading

Hyperliquid supports two broad kinds of trading, and confusing them is an expensive mistake. The safer of the two is spot trading: you buy or sell the actual asset, the way you would swap dollars for euros. If you buy a token on the spot market, you own that token, and the worst case is that its price falls. No leverage, no liquidation, no surprise margin calls.

Perpetual futures — "perps" — are a different animal entirely, and they are what Hyperliquid is best known for. A perpetual is a derivative contract that tracks the price of an asset without ever expiring. You are not buying the asset itself; you are taking a position on which way its price will move. Two concepts make perps dangerous for the unwary:

- Leverage lets you control a position much larger than your deposit. With 10x leverage, a 1,000-dollar deposit controls a 10,000-dollar position. It magnifies gains — and losses — by the same multiple.

- Liquidation is what happens when the market moves against a leveraged position far enough that your deposit (your "margin") can no longer cover the loss. The protocol closes your position automatically, and you can lose your entire margin in minutes. Higher leverage means liquidation is triggered by a smaller price move.

There is also a mechanism called the funding rate, a periodic payment between long and short traders that keeps the perpetual's price tethered to the underlying asset. It is not a fee paid to the exchange, but it is a real cost (or occasional credit) you carry while holding a position. We break the full cost picture down in the fees guide.

High-risk warningLeveraged perpetual futures are among the fastest ways to lose money in crypto. High leverage can wipe out your entire margin from a price move of just a few percent, and it happens automatically — there is no margin call you can answer. Most retail traders who use high leverage lose. Treat this guide as education, never as a recommendation to trade, and never risk money you cannot afford to lose entirely.

How an order actually flows

So what actually happens, step by step, when you place a trade on a non-custodial order-book DEX? Here is the journey from an empty wallet to a settled trade. The exact screens differ from the official app — always follow the official interface — but the logic is consistent.

Connect a self-custody wallet

Instead of signing up with an email and password, you connect a wallet you already control. There is no account creation in the traditional sense — your wallet is your identity. If you are new to this, read our wallet guide first so the custody concept is solid before any money moves.

Deposit funds and set margin

You move collateral into the protocol to back your trades. For perpetuals, this collateral becomes your margin — the cushion that absorbs losses. This step is on-chain, so double-check you are sending the right asset on the right network; sending tokens on the wrong network is a classic, costly first-day error.

Place your order

You choose a market, a direction (long or short), an order type (limit or market) and, for perps, your leverage. A limit order rests in the book until someone matches it; a market order fills immediately against existing orders. Your wallet signs the instruction cryptographically — that signature is your authorisation.

Matching happens on-chain

The order book's matching engine pairs your order with a counterparty whose price crosses yours. Because this runs on Hyperliquid's chain, the matching is recorded on-chain rather than buried in a private server. In principle, anyone can audit that the book behaved as advertised.

Settlement and position management

The trade settles on-chain and your position appears in your account. From here the protocol tracks your margin, applies funding on perps, and will liquidate the position automatically if losses breach your margin. When you are done, you close the position and can withdraw your funds back to your own wallet — no withdrawal approval from any company required.

What makes it different from a custodial exchange

The cleanest way to understand a DEX is to hold it next to the kind of exchange most people start with. The single axis that matters is custody — who actually holds your keys and your money — and it shapes everything else.

A custodial exchange is like a bank. You deposit your assets, and the company holds them on your behalf. The upside is convenience and a safety net: if you forget your password, support can verify your identity and let you back in; you get fiat on-ramps, customer service and, on regulated venues, some consumer protections. The trade-off is trust. You are trusting the company's solvency and security, and it can freeze, restrict or close your account, sometimes with little warning.

A non-custodial DEX like Hyperliquid is like a personal safe. You hold your own keys, and your funds remain under your control at all times. The upside is sovereignty and verifiability: nobody can freeze your balance, and because the order book is on-chain you can verify the system rather than simply trusting it. The trade-off is blunt and unforgiving — there is no support desk and no password reset. If you lose your seed phrase, the funds are gone permanently, and if you approve a malicious contract, no one can claw it back. Convenience is traded for control; control is traded for responsibility.

Neither model is "better" in the abstract — they suit different people and different moments. Many traders sensibly keep one foot in each world: a regulated custodial exchange for buying, learning and cashing out, and a DEX for the trading or transparency a custodial venue cannot offer. Here are the core terms worth keeping straight: